Institutional Insights: Credit Agricole FX Weekly 3/7/26

G10 FX Strategy

Talk Is Cheap; Verbal Intervention Is Overrated

Executive Summary

Fed: Warsh is pushing markets into a world without central-bank forward guidance. Investors must now build policy views from data rather than Fed signalling. That has not stopped markets from pricing more Fed hikes, driven by the idea that the AI capex boom keeps US inflation sticky even as energy falls.

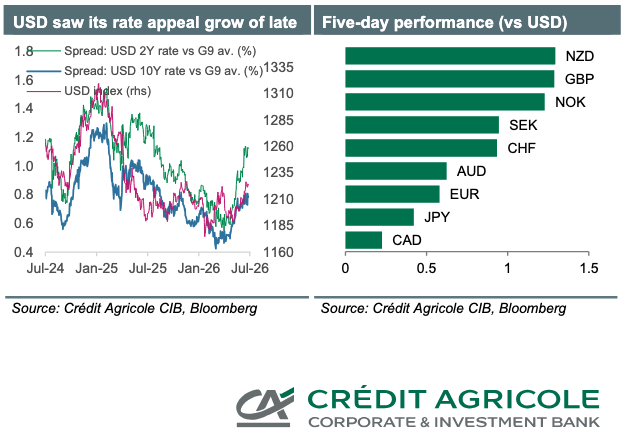

USD: We still think markets are leaning too hawkish on the Fed. A sustained US inflation overshoot is not our base case. The Fed may also tolerate markets tightening financial conditions for it, reducing the need for actual hikes. Near-term USD direction depends on whether US data and risk sentiment validate hawkish pricing.

ECB/EUR: Unlike the Fed, the ECB still uses forward guidance to stress inflation vigilance. But falling energy prices are cheapening that talk, and ECB hike bets have faded. If wider ECB-Fed divergence pushes EUR/USD lower, ECB speakers may become more relevant next week.

JPY: Verbal intervention can continue, but talk alone is unlikely to turn JPY. Actual FX intervention should follow, though timing is uncertain. Because of this uncertainty, the JPY outlook has been downgraded.

CAD: Recent BoC communication has failed to convince markets that the bank will not fall materially behind the Fed. CAD has suffered as a result. The outlook has been downgraded, though next week’s Canadian labour data could challenge bearish positioning.

NZD: RBNZ reluctance to hike has triggered a downgrade to NZD forecasts. Lower oil prices could allow the RBNZ to hold next week in another split decision.

AUD: AUD is losing both rate and commodity-price support. A weaker housing market after tax changes could leave the RBA on hold for the rest of 2026. AUD forecasts have been downgraded.

Key Themes

1. Fed: No Guidance, More Data Dependence, More Market Imagination

Fed Chair Kevin Warsh is forcing investors to prepare for a world without traditional central-bank forward guidance.

His view is simple:

Markets should form policy expectations from economic data.

Central bankers should talk less.

Forward guidance should not be the main policy tool.

But the absence of detailed Fed guidance has not stopped investors from boosting rate-hike expectations.

Instead, markets have filled the vacuum themselves.

The dominant narrative is that the AI-investment boom will keep US inflation sticky, even as global energy prices fall.

That has allowed hawkish Fed pricing to build without much explicit encouragement from the Fed.

Our View

Markets are probably leaning too hawkish on the Fed.

Why?

We do not expect a sustained US inflation overshoot.

Falling energy prices should help.

The Fed may allow rate markets to tighten financial conditions on its behalf.

If markets do the work, actual hikes may not be needed.

This means the Fed can sit back while investors price a more hawkish path.

In practice, market-implied tightening may reduce the need for real tightening.

2. USD: Needs Validation From Data and Risk

The USD outlook now depends on validation.

Markets have already moved toward a hawkish Fed narrative. The next question is whether incoming data justifies it.

Key things to watch:

Services ISM

June FOMC minutes

Next week’s Fedspeak

Global risk sentiment

US inflation signals

If the data remains firm and risk sentiment holds, USD can remain supported.

But if the data fails to validate hawkish pricing, USD upside becomes more vulnerable.

USD bias: Supported near term, but hawkish Fed pricing may be overextended.

Risk: Strong US data validates hike expectations.

Bearish trigger: Softer services/inflation data or risk wobble.

3. ECB: Still Talking, But Markets Are Listening Less

The ECB is taking a different path from the Fed.

Unlike Warsh’s Fed, the ECB still relies on forward guidance to signal inflation vigilance.

ECB speakers continue to stress that they are watching inflation risks and remain ready to act.

But markets are no longer taking the talk at full value.

Falling energy prices have made ECB hawkishness less compelling.

As energy falls, the market sees less need for the ECB to deliver additional hikes. As a result, rate-hike bets have faded.

EUR/USD Implication

If ECB-Fed policy divergence widens further and EUR/USD moves lower, FX investors may refocus on ECB speakers next week.

But for now, ECB talk looks less powerful than Fed-data pricing.

EUR bias: Vulnerable if Fed pricing stays hawkish.

ECB issue: Forward guidance is being cheapened by lower energy.

Watch: ECB speakers next week if EUR/USD downside extends.

4. JPY: Verbal Intervention Is Not Enough

Official verbal intervention in support of JPY can continue near term.

But verbal intervention is usually not enough when the market is driven by:

Wide rate differentials

Weak domestic credibility

Short JPY positioning

USD strength

Actual FX intervention is likely to follow.

The problem is timing.

It is hard to know when authorities will act, and that uncertainty makes JPY positioning difficult.

Because of this, the JPY outlook has been downgraded.

JPY bias: Downgraded; verbal intervention alone is insufficient.

MoF: Actual intervention likely, timing uncertain.

Risk: Intervention sparks sharp but possibly temporary JPY rally.

5. CAD: BoC Talk Fails to Reassure

Recent BoC communication has not reassured markets that the central bank will avoid falling meaningfully behind the Fed.

That has hurt CAD.

Markets are increasingly concerned that:

The Fed may need to stay hawkish.

The BoC may not keep pace.

Canada’s domestic backdrop is weaker.

Lower oil prices reduce CAD support.

As a result, the CAD outlook has been downgraded.

That said, next week’s Canadian labour-market data could push investors to reassess their bearish CAD view.

CAD bias: Downgraded, but data can challenge bearishness.

Watch: Canadian labour-market data next week.

Risk to bearish view: Strong jobs data revives BoC repricing.

6. NZD: RBNZ Foot Dragging Hurts

The RBNZ’s reluctance to hike has led to lower NZD forecasts.

Next week’s meeting is a close call.

Lower oil prices could give the central bank cover to hold off on another hike, potentially in another split decision.

That would reinforce the idea that the RBNZ is reluctant to tighten further.

NZD bias: Downgraded.

RBNZ: Close call next week; lower oil may support a hold.

Risk: Hawkish hike would squeeze NZD shorts.

7. AUD: Losing Rate and Commodity Advantages

AUD is losing support from both sides of its traditional framework:

Rate advantage is fading.

Commodity-price support is weakening.

At the same time, a softer housing market following tax changes could leave the RBA on hold for the rest of 2026.

That combination has led to lower AUD forecasts.

AUD bias: Downgraded.

RBA: Could stay on hold for the rest of 2026.

Drivers: Weaker housing, less rate support, softer commodities.

FX and Gold Outlook

🇪🇺 EUR — Euro

The EUR should continue to trade as collateral damage from global geopolitical risks. We are no longer as bearish on EUR/USD from current levels as before, as we expect additional ECB tightening to limit downside risks to some extent in the coming months.

That said, subdued growth prospects and a loss of international competitiveness should continue to weigh on the appeal of EUR-denominated assets. Potential US tariffs and domestic-demand-driven growth policies in the Eurozone — such as German fiscal stimulus 🇩🇪 — could also hurt Eurozone net exports, reduce corporate demand for the EUR, and keep EUR/USD historically depressed over the longer term.

Despite its recent decline, EUR/USD still looks expensive relative to our long-term fair value model.

🇺🇸 USD — US Dollar

The high-yielding, safe-haven “King of FX” should remain supported, even if geopolitical risks in the Middle East begin to ease. We continue to expect the US economy to outperform many European and Asian economies.

A robust economic outlook and sticky inflation have already lifted Fed policy-rate expectations and strengthened the USD’s rate appeal, although we believe the current market outlook has become too hawkish.

US policy uncertainty could intensify again if fears of fiscal dominance resurface, which may limit future USD gains to some degree. However, the AI boom and the broader US exceptionalism narrative remain intact, likely keeping the USD in demand as unhedged foreign portfolio inflows continue to support the US equity rally. We also expect a pickup in FDI inflows.

Finally, while the USD remains the world’s preeminent reserve fiat currency, de-dollarisation concerns could resurface in the coming months.

🇨🇭 CHF — Swiss Franc

The CHF has reached new decade highs against both the EUR and the USD, supported by sustained safe-haven demand. In response, the SNB has had to strengthen its line of defence against excessive CHF appreciation.

The 0.90 level in EUR/CHF appears to be a line in the sand that the market is willing to respect. A reduction in geopolitical threats and a broader recovery in risk sentiment would likely be needed for the CHF to give up more ground.

🇯🇵 JPY — Japanese Yen

Record levels of intervention have only delayed the rise in USD/JPY, as the US-Japan short-term rate spread has continued to move higher despite the BoJ’s rate hike.

The BoJ has given investors little reason to raise expectations for faster rate increases. While Japan’s economy benefits from a weaker JPY, the authorities must manage both domestic and international political pressures around the currency, leaving intervention still likely.

Intervention could help cap USD/JPY around 164; previously, we expected the cap to be closer to 160.

🇬🇧 GBP — British Pound

We maintain a cautious outlook on GBP/USD from current levels, consistent with our above-consensus view on the USD.

The GBP could remain a pressure valve for anxious market participants concerned about the negative consequences of the leadership change within the Labour Party and the UK government. The currency could also remain vulnerable if persistent stagflation risks fuel concerns about the UK’s economic and fiscal outlook.

However, we believe some of these negatives are already priced into the GBP, especially versus the EUR, given that the Eurozone would also have to deal with the consequences of a negative oil supply shock following the Iran war. We also note that the GBP already looks oversold, while global investors appear underinvested in UK assets.

🇨🇦 CAD — Canadian Dollar

USD/CAD has moved to challenge the upper bound of its 1.35–1.40 range following a more hawkish June FOMC.

The risk that the BoC falls behind the Fed will need to be quickly contained if the range-trading pattern is to remain intact. Evidence of Canada’s macroeconomic resilience could help support this process.

🇦🇺 AUD — Australian Dollar

As investors become more hawkish on the Fed, the AUD is losing its rate advantage at the same time as prices for Australia’s energy and hard-commodity exports are weakening.

A softer domestic housing market, following three rate hikes, as well as tax changes in the Federal Budget, could leave the RBA on hold for the rest of 2026.

🇳🇿 NZD — New Zealand Dollar

New Zealand’s economy is rebounding, while the RBNZ’s monetary policy setting appears too loose. The central bank will likely be forced to correct course.

The RBNZ’s delay in raising rates risks requiring even higher rates over the medium term. New Zealand’s agricultural export prices remain resilient, but El Niño threatens weaker domestic agricultural production.

🇳🇴 NOK — Norwegian Krone

The NOK has given up some ground following the correction in energy prices, although it remains among the best-performing G10 currencies.

Superior carry appeal and Norway’s solid fundamentals should support a renewed appreciation of the NOK in H2 2026, while consolidation may dominate in the near term.

🇸🇪 SEK — Swedish Krona

The SEK has struggled this year after outperforming in 2025.

Risks of a wider policy gap between the Riksbank and the ECB could leave the SEK under pressure in the near term. More convincing evidence of Sweden’s macroeconomic outperformance relative to the Eurozone will likely be needed for the SEK to reverse course later in the year.

🟡 Gold — XAU

We believe many negatives are already priced into gold following its recent sell-off.

Central banks continue to view XAU as a key tool for reducing exposure to the USD, particularly given attempts by the US to weaponize the currency. They could therefore resume gold purchases, especially if the global energy shock continues to fade.

Concerns about fiscal dominance over the Fed could also return, weighing on US real rates and helping gold recover.

Disclaimer: The material provided is for information purposes only and should not be considered as investment advice. The views, information, or opinions expressed in the text belong solely to the author, and not to the author’s employer, organization, committee or other group or individual or company.

Past performance is not indicative of future results.

High Risk Warning: CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 69% and 73% of retail investor accounts lose money when trading CFDs with Tickmill UK Ltd and Tickmill Europe Ltd respectively. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.

Futures and Options: Trading futures and options on margin carries a high degree of risk and may result in losses exceeding your initial investment. These products are not suitable for all investors. Ensure you fully understand the risks and take appropriate care to manage your risk.

Patrick has been involved in the financial markets for well over a decade as a self-educated professional trader and money manager. Flitting between the roles of market commentator, analyst and mentor, Patrick has improved the technical skills and psychological stance of literally hundreds of traders – coaching them to become savvy market operators!